Introduction

Renting a car often comes with an extra question at the counter: “Do you want to add rental car insurance?”

Most travelers either pay extra without thinking or take the risk of saying no. But here’s the secret—many credit cards already include auto rental insurance coverage. Knowing how this benefit works can save you money, time, and stress.

In this guide, we’ll explain how credit card rental car insurance works, which credit cards offer it, and how you can use it the right way.

Cheap Car Insurance: The Ultimate Global Guide to Affordable and Reliable Coverage

how to get insurance to pay for eyelid surgery

Insurance for Churches in Alabama

How Much Is an Ultrasound Without Insurance?

5 Essential Reasons Why Your Business Needs Insurance

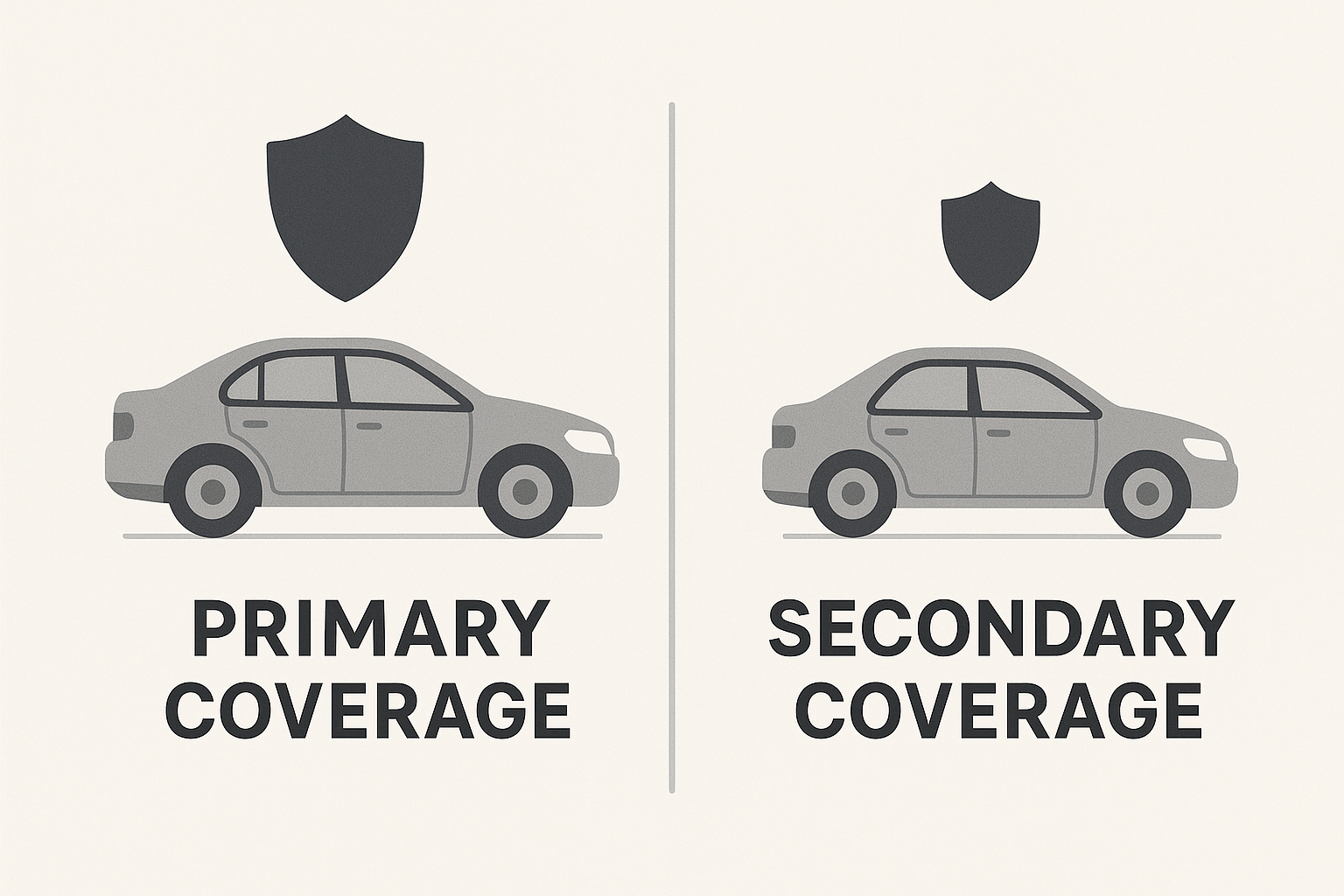

What Is Credit Card Auto Rental Insurance Coverage?

Credit card auto rental insurance is a built-in benefit that covers damage or theft of a rental car when you pay with your credit card. Instead of buying costly insurance from the rental company, your card may already protect you.

This type of insurance is usually offered as:

Primary coverage – Pays first, so you don’t have to file a claim with your personal auto insurance.

Secondary coverage – Kicks in only after your personal insurance pays.

Most basic credit cards provide secondary coverage, while premium travel cards often include primary coverage.

What Does Credit Card Rental Insurance Cover?

Generally, credit card rental insurance includes:

Collision damage (repairs if the car is damaged in an accident).

Theft protection (if the rental car is stolen).

Towing expenses (to the nearest repair facility).

Reasonable loss-of-use charges (when the rental company loses income while the car is being repaired).

What it usually does not cover:

Personal liability for injuries or property damage.

Medical expenses.

Luxury or exotic cars (like Lamborghini or Ferrari).

Trucks, motorcycles, or vans for commercial use.

Rentals longer than 30–45 days.

👉 Always read your card’s “Guide to Benefits” to confirm exact coverage.

Why Use Credit Card Rental Insurance?

Save money – Rental companies charge $15–$30 per day for insurance.

Automatic coverage – No need for paperwork, it activates when you pay with the card.

Peace of mind – Especially useful for frequent travelers who rent cars often.

For many people, this benefit can save hundreds of dollars per trip.

Which Credit Cards Offer Rental Car Insurance?

Most major card networks provide some form of rental coverage, but details differ:

Visa rental car coverage – Many Visa cards provide secondary coverage, but premium Visa cards may include primary.

Visa auto rental insurance – Applies worldwide except restricted countries.

Mastercard – Typically offers secondary coverage.

American Express – Secondary by default, but Amex allows you to buy premium primary coverage for a small fee.

Discover – Coverage is limited; always confirm first.

👉 Example categories of credit cards with auto rental insurance:

Travel rewards cards.

Premium credit cards.

Some everyday cash-back cards (but usually only secondary).

Best Credit Cards for Car Rental Insurance

If you travel often, look for credit cards with primary rental car coverage. These cards handle claims directly, so your personal insurance isn’t affected.

Types of best credit cards for rental car coverage:

Frequent Travelers – Premium travel cards (like Chase Sapphire Preferred/Reserve, Amex Platinum).

Occasional Renters – Mid-level cards with secondary coverage.

Budget-Friendly Option – Some no-fee cards also provide limited protection.

Before applying for a card, always check the coverage guide—don’t assume all cards include it.

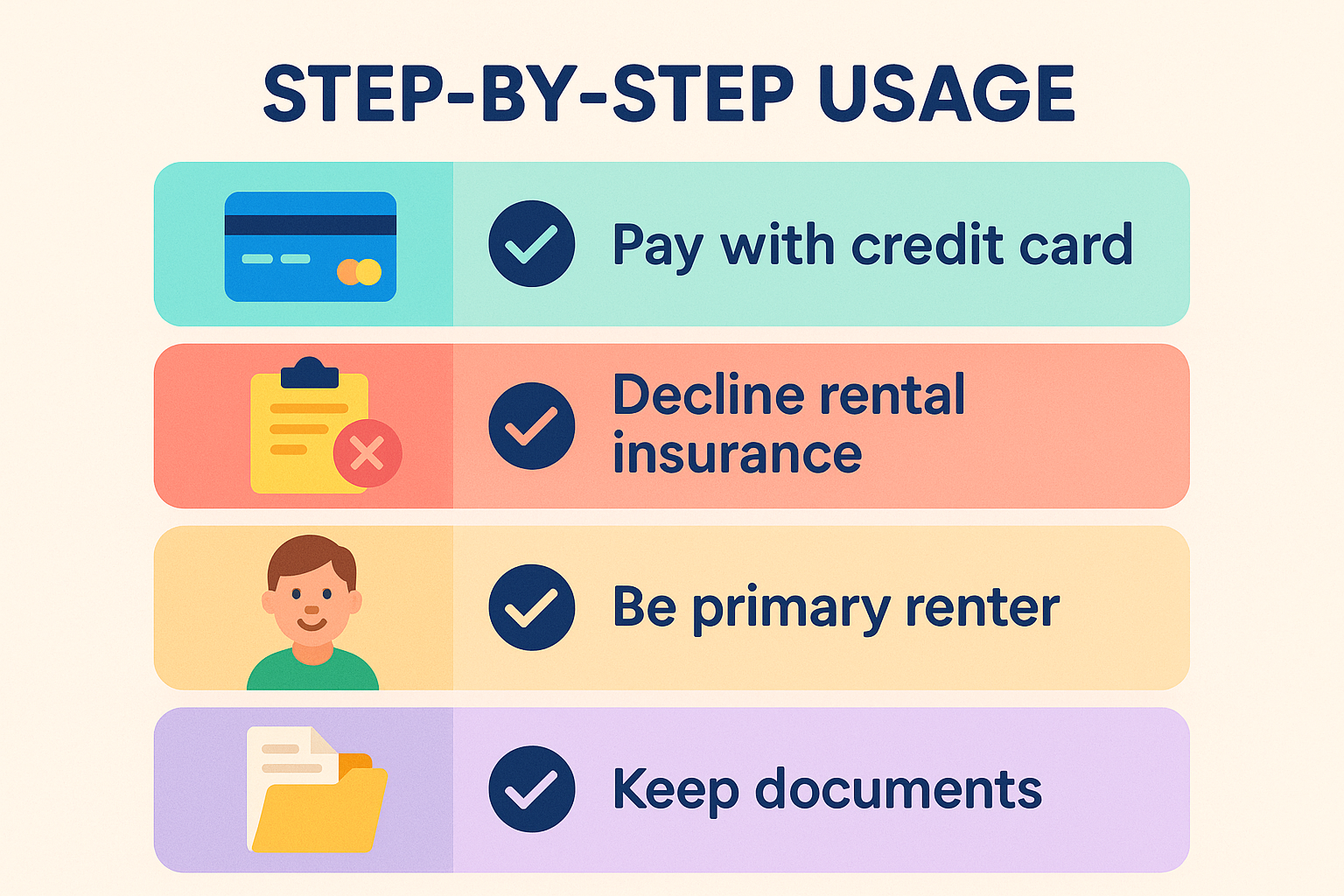

How to Use Credit Card Rental Car Insurance Properly

To activate the benefit, you must follow specific steps:

Pay with your credit card – The entire rental must be charged to the card that offers coverage.

Decline the rental company’s insurance (CDW/LDW) – If you accept it, your card’s benefit usually won’t apply.

Be the primary renter – The cardholder must be listed as the renter.

Keep documents – Carry proof of your credit card benefits (download from your card’s website).

👉 If you damage the car, report it to the rental company immediately and file a claim with your card issuer as soon as possible.

Common Limitations and Exclusions

Credit card auto rental insurance is powerful, but it’s not unlimited. Some common restrictions include:

Countries not covered – Some cards exclude rentals in certain countries.

Vehicle types excluded – Exotic cars, antique cars, large vans, motorcycles.

Duration – Most cards limit coverage to 15–30 days.

Business rentals – Some cards exclude rentals for commercial purposes.

Knowing these limits can prevent surprises when filing a claim.

FAQs About Credit Card Rental Car Insurance

1. Does my credit card cover rental car insurance?

It depends on the card. Most credit cards offer secondary coverage, while a few premium cards offer primary coverage.

2. Which credit cards offer rental car insurance?

Visa, Mastercard, Amex, and Discover may offer it, but benefits vary by card type. Always check your card’s guide.

3. What credit cards cover primary rental car insurance?

Cards like Chase Sapphire Preferred/Reserve are popular for primary coverage.

4. Does Discover card cover rental car insurance?

Discover coverage is limited and may not apply everywhere. Double-check before renting.

5. What is the best credit card for car rental insurance?

It depends on your travel habits. Frequent travelers benefit most from premium travel cards with primary coverage.

6. What does credit card auto rental insurance not cover?

It usually does not cover liability, medical expenses, or luxury/exotic cars.

Final Thoughts

Credit card rental car insurance is a hidden perk that can save you significant money while traveling. But it’s not a one-size-fits-all solution.

Always check whether your card offers primary or secondary coverage.

Read your benefits guide carefully to avoid gaps.

Don’t forget—liability and medical coverage are usually not included.

By understanding your credit card auto rental insurance coverage, you’ll travel smarter, avoid unnecessary costs, and stay protected on the road.