Introduction

Getting a loan is not always easy, especially if you have a poor credit history or no credit score at all. Many traditional banks quickly reject applications when they see a low credit score. This is why people often search for “no credit check loans” or “loans for bad credit.”

But what exactly does a no credit check loan mean? Are they really safe? Can anyone get guaranteed approval? These are common questions borrowers ask when they are in urgent need of money.

This guide will explain everything in simple words—what no credit check loans are, how they work, where you can find them, and the risks you need to be aware of. By the end, you’ll have a clear understanding of your options and how to make smarter financial decisions, even if your credit score is low.

Private Loan Consolidation: The Complete Guide to Student Loan Consolidation and Refinancing

What Does “No Credit Check Loan” Mean?

A no credit check loan is a type of loan where the lender does not run a traditional hard credit check on your credit report before approving your application. Normally, banks and credit unions use your credit score to decide:

-

If they should lend you money.

-

How much money you can borrow.

-

What interest rate you will pay.

In a no credit check loan, the lender skips this process. Instead, they may look at:

-

Your monthly income.

-

Your employment history.

-

Any collateral (like a car or savings).

-

Bank account activity.

👉 This means people with bad credit or no credit history still have a chance to borrow money.

Soft Credit Check vs. Hard Credit Check

It’s important to know the difference:

-

Hard Credit Check: Done by traditional banks when you apply for loans or credit cards. It lowers your credit score temporarily.

-

Soft Credit Check: A lighter review used by some lenders just to verify your identity and background. It doesn’t affect your score.

Many “no credit check” lenders may still perform a soft check, but they will not do a hard inquiry.

Myths About No Credit Check Loans

-

❌ Myth: “Guaranteed approval for everyone.”

✅ Reality: No lender can guarantee approval without looking at your financial situation. If you see this claim, be cautious—it may be a scam. -

❌ Myth: “No risks involved.”

✅ Reality: These loans often come with high interest rates and short repayment periods. -

❌ Myth: “Only for unemployed or desperate people.”

✅ Reality: Many working individuals with steady income also use these loans when banks deny their applications.

Why People Look for No Credit Check Loans

Not everyone who searches for a no credit check loan is careless with money. In reality, many people face situations where traditional banks or lenders refuse to help. Below are the most common reasons why borrowers explore this option.

1. Low or Poor Credit Score

One of the biggest reasons is having a low credit score. If your score is under 600, most banks will automatically reject your loan request. A no credit check loan gives you a chance to borrow money even if your credit history is weak or damaged.

-

✅ Keywords: how to get a loan with low credit score, loans for people with poor credit, can I get a personal loan with bad credit.

2. Bad Credit History

Sometimes, people have missed payments in the past, defaulted on a loan, or even filed for bankruptcy. This creates a negative credit history that stays on record for years. Regular lenders treat such borrowers as “high risk.”

-

A no credit check lender may focus more on your income than your past mistakes.

-

✅ Keywords: how to get a loan with bad credit history, how can I get a loan with bad credit.

3. Urgent Financial Needs

Emergencies do not wait for good credit. Medical bills, car repairs, or sudden rent payments push people to look for urgent loans that don’t require lengthy approval.

-

Some lenders offer same-day or 1-hour payday loans with no credit check, though these usually come with very high fees.

-

✅ Keywords: urgent loans for bad credit, 1 hour payday loans no credit check, no credit check instant loans.

4. Limited or No Credit History

Young professionals, students, or recent immigrants often don’t have a credit history at all. Since banks cannot measure their financial behavior, they deny loan requests.

-

A no credit check loan may be one of the few options available for beginners.

-

✅ Keywords: can you get a loan with no credit, how to get a loan without any credit, no credit score loans.

5. Rejected by Traditional Banks

Many borrowers only turn to no credit check loans after being denied by mainstream lenders. Online lenders, credit unions, and payday lenders sometimes provide smaller loans when banks refuse.

👉 In short: People look for no credit check loans because traditional systems don’t always support borrowers with bad or no credit. While these loans are helpful in emergencies, they also come with risks, which we’ll discuss in later sections.

How to Get a Loan with a Low or Bad Credit Score (Step-by-Step Guide)

Getting a loan when you have bad credit may feel impossible, but it’s not. Many lenders focus on more than just your credit score. If you follow the right steps, you can increase your chances of approval.

Here’s a clear, step-by-step guide:

1. Check Your Credit Report First

Before applying anywhere, get a copy of your credit report. Sometimes mistakes—like wrong late payments or closed accounts—hurt your score. If you fix these errors, your chances of approval improve immediately.

-

Free credit reports are available once a year in most countries.

-

Even if your score is low, knowing the number helps you prepare.

✅ Keywords: how to get a loan with low credit score, how to get a loan with poor credit.

2. Compare Lenders Who Work with Bad Credit

Not every bank or lender accepts bad credit borrowers. Instead of applying everywhere and getting rejected, look for lenders who specifically advertise loans for people with bad credit or no credit.

-

Credit unions, online lenders, and community banks often give more flexibility.

-

Some fintech companies only focus on borrowers with limited or no credit.

✅ Keywords: how can I borrow money with bad credit, loans for people with poor credit.

3. Show Proof of Income

When credit is weak, lenders want to see stability in other areas. If you can show that you have a regular job or steady income, your chances rise.

-

Prepare recent pay stubs, bank statements, or tax returns.

-

Even gig workers (freelancers, delivery drivers, etc.) can qualify if income is stable.

4. Apply with a Co-Signer

A co-signer is someone with good credit who agrees to take responsibility if you can’t repay. Having one can:

-

Reduce interest rates.

-

Improve approval chances.

-

Help you qualify for larger amounts.

5. Offer Collateral (Secured Loan Option)

Some lenders allow you to use assets like your car, savings account, or jewelry as security. This reduces the lender’s risk and increases your chance of approval.

-

Example: A secured personal loan using a vehicle title.

-

Be careful—if you fail to repay, the lender can take your asset.

6. Borrow Smaller Amounts First

Instead of applying for a $20,000 loan immediately, start with a smaller amount ($1,000–$5,000). Proving that you can repay on time builds trust with the lender and improves your credit score over time.

✅ Keywords: 1000 loan bad credit, 2000 loan bad credit, 5000 loan bad credit.

7. Apply Online for Faster Approval

Many online lenders give quick approvals, sometimes within hours, without a hard credit check. They may charge higher fees, but if you need urgent money, this can be useful.

✅ Keywords: online no credit check loans, no credit check instant loans.

👉 By following these steps, you can significantly increase your chances of getting a loan even with bad credit. The key is to show income stability, borrow responsibly, and avoid scams that promise guaranteed approval.

Types of Loans Available for Bad Credit or No Credit

Not all no credit check loans are the same. Depending on your financial situation, income, and needs, you can choose from different types of loans. Each option has its own benefits and risks. Let’s break them down one by one.

1. Personal Loans for Bad Credit

Some lenders specialize in offering personal loans to borrowers with poor credit. These are usually installment loans that you repay in fixed monthly payments.

-

Loan amounts can range from $1,000 to $50,000 depending on income.

-

Interest rates are higher compared to borrowers with good credit.

-

If you make payments on time, these loans can help improve your credit score.

✅ Keywords: personal loans for bad credit guarantee approval, can I get a personal loan with bad credit.

2. Payday Loans Without Credit Check

Payday loans are short-term loans, usually between $100 and $1,000, that must be repaid by your next payday.

-

Very easy to qualify for, since lenders only check your income.

-

Extremely high fees and interest rates (sometimes over 300% APR).

-

Risk of getting trapped in a cycle of debt if you cannot repay on time.

✅ Keywords: payday loans without credit check, 1000 loan bad credit, 1 hour payday loans no credit check.

3. Installment Loans for Bad Credit

Unlike payday loans, installment loans allow you to repay in multiple fixed payments over months or years.

-

More manageable than payday loans.

-

May require collateral (like a car title).

-

Better for larger amounts such as $2,000 or $5,000 loans.

✅ Keywords: 2000 loan bad credit, 5000 loan bad credit, extremely bad credit loans.

4. Credit Union Loans

Credit unions are nonprofit organizations that often provide loans with lower interest rates than banks. They are more flexible with borrowers who have poor credit.

-

Membership may be required.

-

Approval depends more on your relationship and income than credit score.

-

Great option if you want lower fees and better terms.

✅ Keywords: loans for people with poor credit, no credit score loans.

5. Secured Loans (Collateral-Based)

If you own valuable assets, you can get a loan by putting them up as collateral. Examples include car title loans, savings-secured loans, or home equity loans.

-

Easier approval because lender takes less risk.

-

Larger loan amounts possible (even up to $50,000).

-

Risk: You may lose your asset if you default.

✅ Keyword: how to get a 50000 loan with bad credit.

6. Online No Credit Check Loans

Today, many fintech lenders operate fully online. They provide quick applications, same-day approvals, and funds directly to your bank account.

-

Faster than banks and credit unions.

-

May still perform a soft credit check.

-

Be cautious of fake lenders online.

✅ Keywords: online no credit check loans, no credit check instant loans, urgent loans for bad credit.

👉 In short: Borrowers with bad or no credit have multiple loan options—personal loans, payday loans, installment loans, credit union loans, secured loans, and online loans. Choosing the right type depends on how much money you need, how fast you need it, and how quickly you can repay.

Where Can You Get a Personal Loan with No or Bad Credit?

If your credit score is low, you might think that banks are your only option—but that’s not true. Today, there are many types of lenders who can provide loans for people with bad credit or no credit history. Each option comes with pros and cons.

1. Traditional Banks

-

Pros: Trusted institutions, larger loan amounts, regulated by law.

-

Cons: Strict credit score requirements; most banks reject borrowers with poor credit.

-

Best if you already have a long-term relationship with the bank.

2. Credit Unions

Credit unions are smaller, community-based financial organizations. They often consider your overall financial picture instead of just your credit score.

-

More flexible than banks.

-

Usually charge lower interest rates.

-

May require you to become a member before applying.

✅ Keywords: where can I get a personal loan with no credit, loans for people with poor credit.

3. Online Lenders

Online lending platforms are becoming very popular. They usually have quick applications and fast approvals (sometimes within 24 hours).

-

Some specialize in bad credit loans.

-

Funds go directly to your bank account.

-

Watch out for scammers—always choose well-known companies.

✅ Keywords: online no credit check loans, no credit check instant loans.

4. Peer-to-Peer (P2P) Lending Platforms

These platforms connect borrowers directly with individual investors. Instead of a bank lending you money, regular people or groups invest in your loan.

-

Flexible approval standards.

-

Competitive rates for certain borrowers.

-

Availability depends on your country.

5. Payday Lenders and Cash Advance Services

These lenders give very small amounts (like $500–$1,000) with no credit check.

-

Fast approval, sometimes in an hour.

-

Extremely high interest rates and fees.

-

Should only be used as a last resort.

✅ Keywords: where can I get a loan with horrible credit, 1 hour payday loans no credit check.

👉 Bottom line: If you need a personal loan with bad or no credit, your best options are usually credit unions and online lenders. Payday lenders may give fast cash, but they should be used carefully because of high costs.

No Credit Check Loans Guaranteed Approval – Reality or Scam?

When searching online, you will often see ads that promise:

-

“No credit check loans guaranteed approval!”

-

“Instant cash, no questions asked!”

These headlines sound attractive, especially if you have bad credit. But the truth is: there is no such thing as a 100% guaranteed loan approval.

Why “Guaranteed Approval” is a Red Flag

Legitimate lenders always need to check something before lending money. Even if they don’t run a hard credit check, they will usually ask for:

-

Proof of income.

-

Employment details.

-

Bank account history.

If a lender says you don’t need to provide anything at all and approval is “guaranteed,” it is a strong warning sign of a scam.

The Risks of “Guaranteed Approval” Loans

-

Extremely High Interest Rates

-

Some payday lenders charge APRs of 200% to 500%, making it almost impossible to repay.

-

-

Hidden Fees

-

Application fees, late fees, and rollover charges quickly add up.

-

-

Debt Trap

-

Many borrowers end up borrowing again just to repay the first loan, falling into a cycle of endless debt.

-

-

Scammers Stealing Personal Data

-

Fraud websites may use “guaranteed loan” offers to steal your identity, bank details, or social security number.

-

How to Spot a Scam

-

🚩 The lender asks for upfront payment before giving the loan.

-

🚩 The website has no physical address or customer service number.

-

🚩 Promises of “approval for everyone” without checking income.

-

🚩 Unsecure website (no HTTPS).

Safer Alternatives to “Guaranteed Approval”

If you truly need a loan but want to stay safe:

-

Choose credit unions or community lenders.

-

Use online lenders with real reviews.

-

Consider secured loans where you use an asset as collateral.

-

Explore credit-builder loans to improve your score for the future.

✅ Keywords: no credit check loans guaranteed approval, no credit check instant loans, 1 hour payday loans no credit check.

👉 The truth: No lender can guarantee approval without any checks. If you see such a promise, be cautious—it’s either very expensive or a scam.

How to Get Large Loans with Bad Credit (e.g., $50,000 Loan)

Borrowing a small loan of $500 or $1,000 with bad credit is possible. But what if you need a large loan, like $50,000? This is much more challenging, but not impossible. Lenders take extra precautions before giving out such big amounts.

1. Understand the Requirements

Large loans require more than just a basic application. Even if a lender doesn’t run a hard credit check, they will carefully examine:

-

Your income level – Do you earn enough to make monthly payments?

-

Your debt-to-income ratio (DTI) – How much debt do you already have compared to your income?

-

Collateral value – If you put up an asset, is it worth the loan amount?

2. Use Collateral (Secured Loans)

Most people with bad credit can only qualify for a large loan by offering something valuable as collateral, such as:

-

A car, truck, or other vehicle.

-

A home or property (home equity loan).

-

Savings account or certificate of deposit.

Collateral reduces risk for the lender and makes them more willing to approve a big loan.

✅ Keyword: how to get a 50000 loan with bad credit.

3. Apply with a Co-Signer

Having a co-signer with good credit can make a huge difference. Lenders see it as extra security since the co-signer promises to repay if you cannot. With a co-signer, you may even get lower interest rates.

4. Show Stable and High Income

If you’re applying without collateral or a co-signer, you must prove that your income is high enough to handle monthly payments on a $50,000 loan.

-

Provide recent pay stubs, tax returns, or business income records.

-

The more stable your income looks, the better your chances.

5. Consider Peer-to-Peer or Specialized Lenders

Some P2P platforms and online lenders focus on higher loan amounts. They may be more flexible than banks, but you’ll need to prove you can handle repayment.

6. Improve Your Application

Even with bad credit, you can make your application stronger by:

-

Reducing your other debts before applying.

-

Borrowing a smaller loan first, then applying for a larger one later.

-

Writing a short explanation of your financial situation (many lenders appreciate transparency).

👉 Bottom line: Getting a $50,000 loan with bad credit is difficult but possible if you use collateral, a co-signer, or show strong income stability. Without these, approval is highly unlikely.

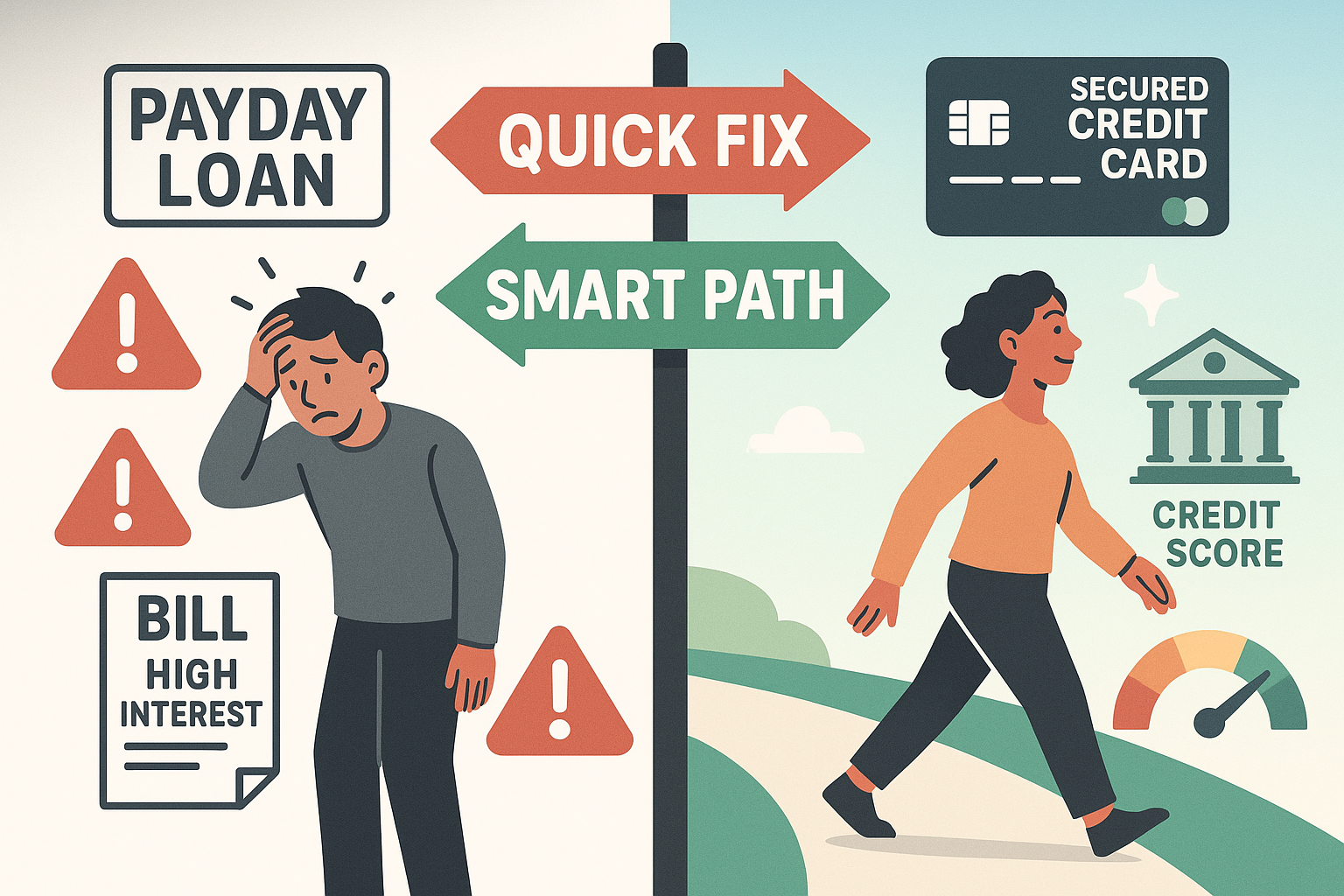

Alternatives to No Credit Check Loans

While no credit check loans sound easy, they are often expensive and risky. Before applying, it’s smart to explore safer options that may cost less and improve your financial health in the long run.

Here are some alternatives to consider:

1. Borrow from Family or Friends

-

This is the most common alternative when banks say no.

-

Family or friends may lend you money without interest or strict terms.

-

Be sure to write down an agreement to avoid misunderstandings later.

2. Negotiate with Creditors

If you need money to pay bills, sometimes you don’t need a new loan at all. Instead:

-

Contact your utility company, landlord, or hospital.

-

Ask for a payment plan, extension, or reduced settlement.

-

Many creditors would rather work with you than see you miss payments.

3. Side Income or Emergency Fund

If you can’t get affordable credit, another option is to boost your cash flow.

-

Take freelance jobs, part-time work, or gig economy tasks (delivery, ridesharing).

-

Sell unused items online for quick cash.

-

Build a small emergency fund for the future.

4. Credit-Builder Loans

These are small loans designed specifically to build your credit score.

-

The lender keeps the money in a savings account while you make payments.

-

Once the loan is paid off, you get the funds and a stronger credit history.

-

This improves your chances of qualifying for larger, cheaper loans later.

5. Secured Credit Cards

If you don’t qualify for a regular credit card, a secured card is a good start.

-

You pay a refundable deposit (e.g., $200–$500).

-

That deposit becomes your credit limit.

-

Using it responsibly helps build credit quickly.

6. Local Assistance Programs

Some nonprofit organizations, community centers, and government agencies provide:

-

Small emergency loans.

-

Housing or rental support.

-

Grants for medical or utility expenses.

These options may be free or very low-cost compared to payday loans.

👉 In short: Before jumping into a no credit check loan, always explore family help, creditor negotiation, side income, or credit-builder products. These choices may save you money and protect you from high-interest debt traps.

Tips to Improve Your Loan Approval Chances

Having bad or no credit doesn’t mean you’ll never get approved for a loan. By taking some smart steps, you can increase your chances of getting accepted and possibly secure better terms.

1. Show Proof of Stable Income

-

Lenders want to see that you can repay the loan.

-

Keep documents ready like pay stubs, bank statements, or tax returns.

-

Even gig workers and freelancers can show digital payment records as proof.

2. Reduce Your Debt-to-Income (DTI) Ratio

-

DTI compares your monthly debt payments to your monthly income.

-

Example: If you earn $2,000 per month and pay $800 in debt, your DTI is 40%.

-

Lenders prefer a lower DTI (ideally under 35%).

-

Pay down small debts before applying to boost your chances.

3. Use a Co-Signer

-

A co-signer with good credit can apply with you.

-

Their strong credit history helps you qualify for a loan and possibly a lower interest rate.

-

Make sure your co-signer understands the responsibility — they’ll also be liable for missed payments.

4. Offer Collateral (Secured Loans)

-

Secured loans use assets like a car, savings account, or property as security.

-

Collateral reduces the lender’s risk, so approval chances go up.

-

Just be careful: If you miss payments, the lender can take your asset.

5. Apply to the Right Lenders

-

Not all lenders treat bad credit the same.

-

Community banks, credit unions, and online lenders are often more flexible.

-

Check eligibility requirements before applying so you don’t waste hard credit checks.

6. Start Small

-

Instead of applying for a $20,000 loan right away, start with smaller amounts ($500–$2,000).

-

Repay on time and build trust.

-

Many lenders may increase your borrowing limit after a positive repayment history.

👉 By preparing in advance with these tips, you’ll stand out as a lower-risk borrower, even if your credit history isn’t perfect.

Risks of No Credit Check Loans

No credit check loans may look like a quick solution, but they come with serious downsides. Before applying, it’s important to understand the risks.

1. Extremely High Interest Rates

-

Many no credit check loans charge APR between 100%–400% or more.

-

This means if you borrow $500, you could end up repaying $1,500–$2,000 in just a few months.

-

High interest makes it very hard to escape debt.

2. Hidden Fees

-

Lenders often add processing fees, late fees, rollover charges, or prepayment penalties.

-

These extra costs can make the loan even more expensive than it first appeared.

3. Short Repayment Terms

-

Most payday or instant loans require repayment in 2–4 weeks.

-

If you can’t pay on time, you may need to renew or “roll over” the loan, adding more fees and interest.

4. Risk of a Debt Cycle

-

Borrowers often take a new loan to pay off the old one.

-

This creates a cycle of debt where you’re constantly paying fees without reducing the principal.

5. Impact on Your Finances

-

Even though lenders don’t check your credit score, unpaid loans may still be reported to collections.

-

Debt collectors can add stress and damage your long-term financial health.

6. Risk of Losing Collateral

-

Some “no credit check” loans are secured loans backed by your car or savings.

-

If you default, the lender can take your asset, leaving you worse off than before.

👉 In short: No credit check loans may solve today’s problem but create bigger financial challenges tomorrow. Always think carefully before committing.

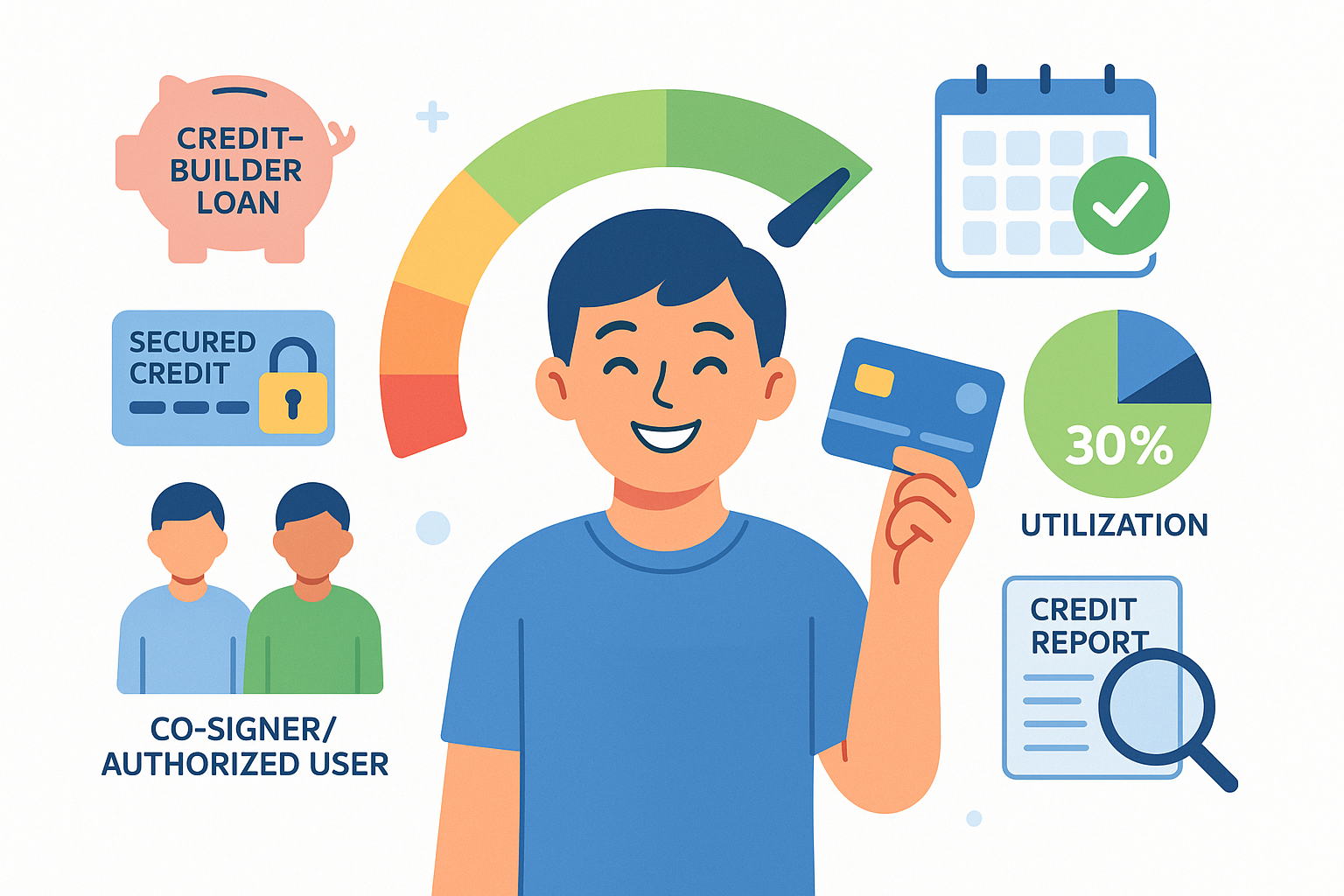

Safer Strategies to Build Credit Over Time

Instead of relying on costly no credit check loans, focus on building your credit. A better credit score opens doors to affordable personal loans, credit cards, and even mortgages. Here’s how you can start:

1. Apply for a Credit-Builder Loan

-

These small loans are offered by credit unions and community banks.

-

The money is kept in a savings account until you finish payments.

-

After repayment, you get both the funds and a stronger credit history.

2. Use a Secured Credit Card

-

Deposit a set amount (e.g., $200–$500) as security.

-

That amount becomes your credit limit.

-

Use it for small purchases and pay off the balance every month.

-

This builds positive payment history, a key factor in credit scores.

3. Pay Bills on Time

-

Payment history makes up 35% of your credit score.

-

Even one late payment can damage your score.

-

Use reminders or automatic payments to stay on track.

4. Keep Credit Utilization Low

-

Credit utilization = how much of your credit limit you use.

-

Try to stay under 30% of your available credit.

-

Example: If your card limit is $1,000, keep spending below $300.

5. Consider a Co-Signer or Authorized User

-

If someone with good credit co-signs your loan, their positive history helps you.

-

Or, become an authorized user on a trusted person’s credit card.

-

Their good habits boost your score without extra risk.

6. Monitor Your Credit Reports

-

Check reports from Experian, Equifax, and TransUnion regularly.

-

Look for errors and dispute them if needed.

-

Many free apps allow you to track your credit score monthly.

👉 By slowly improving your credit, you won’t need to rely on expensive no credit check loans in the future. Instead, you’ll qualify for lower rates, better terms, and higher loan amounts.

(FAQ) About No Credit Check Loans

1. Can I really get a loan with no credit check?

Yes, some lenders offer loans without checking your credit. But keep in mind — they often come with very high interest rates and fees. Always compare options before applying.

2. Are “guaranteed approval” loans real?

No lender can promise 100% guaranteed approval for everyone. If a site claims this, it may be a scam. Legit lenders will at least verify your income and repayment ability.

3. How fast can I get a $1,000 loan with bad credit?

Some online lenders and payday loan providers offer same-day or even 1-hour approvals. However, these loans are expensive. Credit unions or online installment lenders may take longer but offer safer terms.

4. What is the difference between no credit and bad credit?

-

No credit means you’ve never borrowed before and have no history.

-

Bad credit means you borrowed but had late payments or defaults.

Both situations are risky for lenders, but no credit is sometimes easier to fix.

5. Do no credit check loans affect my credit score?

Yes. Even if approval didn’t require a credit check, missed payments may still be reported to credit bureaus, lowering your score further. Timely repayment, however, can sometimes improve your credit.

Conclusion

No credit check loans may seem like a quick fix when you’re facing financial stress, but they come with high interest rates, short repayment terms, and hidden risks. For people with bad or no credit, these loans can sometimes make problems worse instead of solving them.

The smarter path is to explore safer alternatives — like credit unions, secured cards, or credit-builder loans — while working on improving your credit score over time. Building good financial habits will not only give you access to better loan options but also help you avoid falling into a cycle of debt.

At the end of the day, the best loan is the one that helps you move forward without putting your future at risk.

✅ Key Takeaway:

-

Use no credit check loans only as a last resort.

-

Focus on credit-building strategies for long-term financial health.

-

Explore community banks, credit unions, and online installment lenders before payday loans.

👉 If you found this guide helpful, explore our other resources on personal finance, loans, and credit improvement strategies to make confident money decisions.